From January 1, 2023, all medium and large taxpayers in Romania must submit their accounting and tax records electronically via the SAF-T system. The Standard Audit File (SAF-T) is an international XML standard for filing tax returns.

ANAF, Romania’s National Agency for Fiscal Administration, requires companies to attach their SAF-T D406 form in PDF files.

Many European countries, including Romania, have adopted the SAF-T standard for the electronic exchange of tax and accounting information. The Romanian name for SAF-T is D406 Informative Declaration.

Introducing the Romanian SAF-T D406 Informative Declaration is an important step in improving transparency and accountability regarding tax compliance.

It will also help taxpayers to exchange information with tax authorities across countries.

This guide will answer questions on what the Romanian SAF-T returns contain, implementation and reporting timelines, and how to prepare for SAF-T.

Let’s get to it.

What is a Standard Audit File (SAF-T)?

Standard Audit File for Tax (SAF-T) is an internationally recognized tax reporting standard that simplifies submitting tax information to tax authorities. The electronically transmitted file contains accounting and tax information, allowing tax authorities to review the taxpayer’s operations.

The Organization for Economic Co-operation and Development (OECD) defined the SAF-T system in 2005, which requires taxpayers to express their information in XML.

However, the OECD allows national tax authorities to develop their policies for representing SAF-T files, including choosing their data formats and adding elements.

The SAF-T system aims to standardize data exchange to make it easier for tax authorities to audit companies because they can easily access a company’s tax and accounting records electronically.

It also reduces the administrative burden for companies as they can automate the process with the right system and do away with papers. In addition, the data exchange system guarantees information security.

Read more: E-invoice Formats Explained: A Comprehensive Guide to All Types (In-Depth Analysis)

What’s the timeline for the implementation of SAF-T for tax in Romania?

From January 1, 2023, all companies in the medium and large taxpayer categories must declare their tax information in Romania’s recognized SAF-T file, form D406. Small taxpayers have until January 1, 2025 to implement SAF-T for declaring tax information.

The Romanian tax authority, National Agency for Fiscal Administration (ANAF), officially commenced the SAF-T tax reporting requirement in January 2022. It is compulsory for all resident companies and foreign companies with a Romanian VAT registration number.

However, the SAF-T implementation timeline depends on the taxpayer’s tax category.

- Jan 1, 2022 - large taxpayers in this category as of Dec 31, 2021

- July 1, 2022 - large taxpayers who were not in the category as of Dec 31, 2021

- Jan 1, 2023 - medium taxpayers in this category as of Dec 31, 2022

- Jan 1, 2023 - all financial institutions and insurance and reinsurance firms categorized as large taxpayers as of Dec 31, 2021

- Jan 1, 2025 - small taxpayers

- Jan 1, 2025 - non-resident taxpayers with Romanian VAT registration numbers

The Romanian SAF-T declaration is part of a larger effort by the government to ensure greater transparency within its taxation system.

ANAF has released detailed guidance on the data structure required for submission to help companies comply with the new regulation.

Romania’s version of the SAF-T is the D406 form, which is an XML attachment in a PDF. It contains over 390 mandatory accounting and tax elements that taxpayers should declare.

Romanian tax authorities will use the information in the SAF-T file during tax inspections to verify that the filed tax returns match the taxpayer’s accounting records.

Taxpayers reporting value-added-tax (VAT) obligations will submit their SAF-T D406 forms monthly or quarterly.

In contrast, taxpayers with a non-calender tax year and those without VAT obligations will submit their tax files quarterly.

Read more: Request our free E-invoicing Compliance Timeline

What are Romanian SAF-T returns?

The Romanian SAF-T standard is based on the OECD’s SAF-T version 2.0. It is called D406 Informative Declaration, which is an XML file. ANAF requires taxpayers to attach their XML-formatted D406 forms in a PDF file before submitting them.

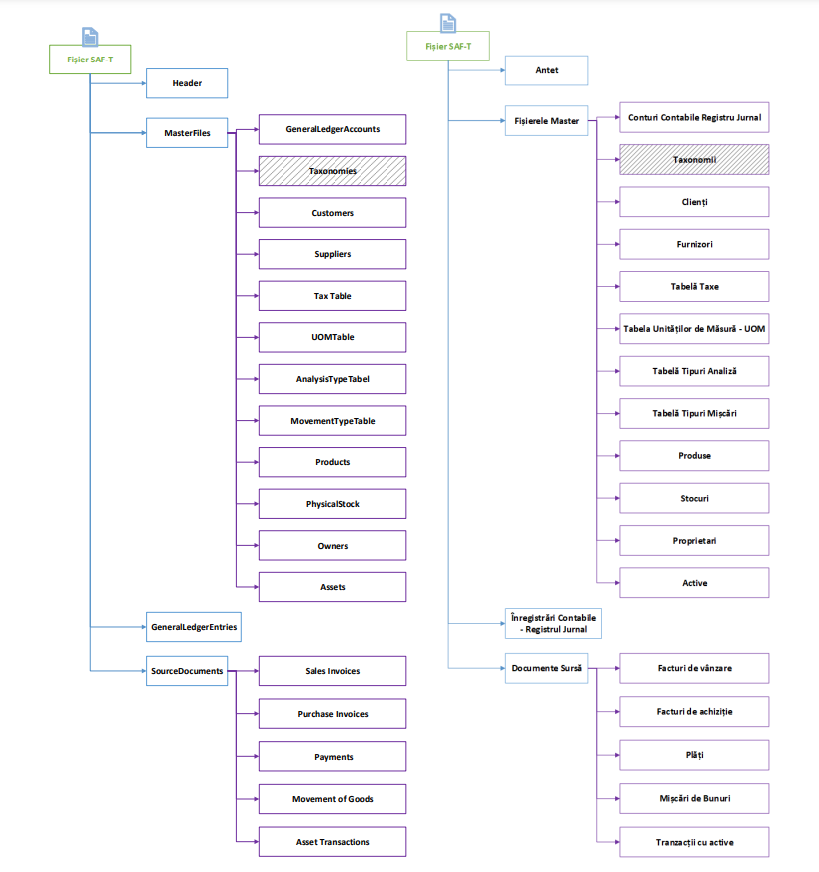

The D406 Informative Declaration has four main sections:

- Header - contains information about the company name, address, and registration number

- MasterFiles - contains information about customers, suppliers, tax codes, products, assets, physical stock, and general ledger accounts, among others.

- GeneralLedgerEntries - contains accounting information (should be in line with the Romanian Chart of Accounts)

- SourceDocuments - this is where you submit sales invoices, purchase invoices, payments, asset transactions, and movement of goods.

Each main section has subsections, which have more subsections, resulting in hundreds of fields you need to report in detail.

In addition, most fields in the SAF-T files only accept defined values, so you’ll need to map your tax and accounting information from your ERP to the corresponding fields.

For example, you need to use the correct VAT tax codes and match invoices with their defined codes.

In addition, the General Ledger entries should align with the account numbers provided in the Romanian Chart of Accounts.

How to submit Romanian SAF-T returns

ANAF provides the DUKIntegrator tool for validating the XML files and generating the corresponding PDF file with the attachment. But they don’t provide a tool for generating XML files.

Taxpayers must partner with third-party solutions like Storecove to retrieve data from their ERP systems and generate XML files.

After generating the PDF file with an attached XML, taxpayers must sign it digitally with a qualified digital certificate. They can then submit the declaration to ANAF by uploading it on the E-Guvernare website.

After successful submission, taxpayers will receive a SAF-T receipt confirmation.

The D406 form cannot exceed 500 MB. If your statement exceeds the limit, you can submit it in several portions.

SAF-T Romania submission deadlines

The National Agency for Fiscal Administration (ANAF) demands three types of SAF-T D406 statements:

- D406 Informative Statement for VAT purposes - to be submitted monthly or quarterly by the last calendar day of the month following the taxpayer’s VAT reporting period.

- D406 Informative Statement for Fixed Assets - to be submitted annually within the deadline for submitting the financial statements.

- D406 Informative Statement for Stocks - to be submitted upon request by tax authorities, but not earlier than 30 calendar days after receiving the request.

Fortunately, taxpayers have reporting grace periods that run from the last day of the tax reporting period.

Monthly reporting taxpayers get a 6 month grace period for the 1st declaration, a 5 month grace period for the 2nd declaration, 4 months for their 3rd declaration, 3 months for the 4th declaration, and a 2 month grace period for the 5th declaration.

In contrast, quarterly reporting taxpayers get a 3 month grace period for submitting their first tax declaration.

Taxpayers who fail to submit their SAF-T D406 within the statutory deadlines will be subject to non-compliance penalties.

The same applies to taxpayers who submit incomplete or incorrect SAF-T files unless they correct them within the deadlines.

Those who submit their D406 forms with errors can submit rectifying statements.

Who will need to use SAF-T for tax in Romania?

The SAF-T obligation applies to all Romanian VAT taxpayers, including foreign entities registered for VAT in Romania.

The following legal entities will need to use SAF-T for tax in Romania:

- Joint-stock companies (SA, SNC) and Joint-stock limited companies (SCA)

- Simple limited companies (SCS) and limited liability companies (SRL)

- National Societies/Companies

- National research and development organizations

- Craft cooperative organizations (OC1), Credit cooperative organizations (OC3), and consumer cooperative organizations (OC2)

- Associations with or without a patrimonial purpose

- Autonomous governments

- Investment bodies collective without a constitutive act, privately administered and optional pension funds, and other entities organized based on the Civil Code

- Legal entities based abroad without legal personality in Romania

- Foreign legal entities with permanent headquarters in Romania

- Foreign legal entities that have the place of effective management in Romania

- Non-resident companies that have a VAT registration code in Romania (taxpayers registered through direct registration or fiscal representatives and fixed offices)

Who does not need to use SAF-T?

- Authorized natural persons (PFA) and natural persons conducting profit-making activities (PFL)

- Sole proprietorships (II) and sole proprietorships with limited liability (URL)

- Family enterprises (IF) and family associations (ASF)

- Individual medical offices (CMI)

- professional associations of lawyers with limited liability (SPAR) and individual lawyers

- Professional notarial societies and individual notarial offices

- Professional Societies Insolvency Practitioners (SPI)

- Public institutions (PUB)

- Administrative authorities

With adequate preparation, businesses can ensure they comply with the new regulations, which will help protect their finances and reputation in the long run.

The businesses will need to invest in systems or software to generate SAF-T reports and manage this data efficiently and securely.

Companies serving different jurisdictions should also consider how they’ll manage reporting obligations in multiple jurisdictions and develop plans to ensure compliance with each country’s requirements.

How Romanian companies can get ready for SAF-T

Understanding the requirements of Romania’s SAF-T D406 Informative Declaration is essential for any obliged taxpayer. Beyond extracting ERP data, companies must understand what data they need to report, how to format it, and when to submit it.

Companies must also update their accounting software to adhere to Romanian tax regulations.

Additionally, business leaders should consult with an e-invoicing software solutions provider experienced in accounting automation and SAF-T compliance to ensure your business has the tools for success when Romania’s SAF-T Declaration becomes mandatory.

Get ready for SAF-T with an e-invoicing solution

Medium taxpayers should have a SAF-T system in place before January 1, 2023, especially if they must submit a D406 Informative Declaration monthly for VAT purposes. Small taxpayers can also stay ahead of the implementation deadline by getting their SAF-T submission system in place.

While filing the D406 forms involves filling hundreds of fields with great attention to detail, companies don’t need to do this manually every month. Instead, they can take advantage of e-invoicing solutions that automate the entire process.

It’s the easiest way to ensure compliance when generating lots of accounting data and reporting it as needed.

Speak with a tax expert today to learn how we can help with SAF-T reporting compliance.

More information about Romanian SAF-T Declaration Becomes Compulsory in 2023

Contact us for more information or schedule a consult with one of our e-invoicing experts.

Read also:

Comments